It is not the first time that President Trump's rhetoric seems convoluted when discussing economic issues. So far, his confusion has been mainly on trade. I have

pointed here the mistakes in his reasoning. And after beginning to experience the negative consequences of his trade war, Americans are once again shifting towards favoring free trade. According to a recent

NBC/WSJ poll, the share of Americans who believe that free trade is good has risen from a little over 50% in 2015 to an all-time high of 64% in August 2019, while the share of those who hold negative views has fallen from a little over 40% to 27%. By unwillingly illustrating the perils of defying economic theory, Trump may be the most effective ally that mainstream economists have. A slow-down in economic activity would be bad for reelection however, so Trump seems to be looking for someone to throw under the bus if the negative consequences of his trade policies intensify. In

today's press conference, he asserted that our economic growth will continue unless the Fed kills it. The growth is, of course, the President's doing, but a recession would be the Fed's doing. How convenient! What is the Fed's sin? That they raised interest rates too fast, are keeping them too high, and are normalizing. The President wants the Fed to gradually lower the targeted interest rate by "a minimum" of 100 basis points (one percentage point). He believes that if the Fed did that, we would experience a "burst of growth that we have never seen before". What is wrong with his assertions? Well, there are factual problems and theoretical ones.

Let's start with whether monetary policy is "too tight". There is an excellent and more detailed analysis by Stephen Williamson

here, so I will only mention a few facts. Below is a graph showing the Federal Funds Rate (FFR) since January 1990. The FFR is the rate at which banks borrow reserves from each other overnight, and is the rate that the Fed has traditionally targeted. The graph extends to July 2019, when the FFR stood at 2.40%. As you can see, by historical standards this is remarkably low, especially given that the economy is experiencing reasonable growth and a tight labor market; the unemployment rate is at 3.7% and the rate of job vacancies relative to the rate of unemployment is quite high. As well, keep in mind that the Fed recently lowered the targeted range further, to between 2% and 2.25%. Lowering the FFR by 100 basis points below the current range would bring it below the rate of inflation, which is currently 1.8%, and lead to a negative real rate unless inflation also declines. There is no justification for such a dramatic move. Moreover, as Williamson shows, the Fed's balance sheet remains much larger than it was before the financial crisis. So no, we are not even close to normalization.

As far as economic theory goes, obviously the President is unaware of the concept of monetary neutrality. While economists disagree on whether money is neutral in the short run, the consensus is that money is neutral in the long run, and that sustained growth can only come from real factors like improvements in productivity. In other words, most economists believe that even if a positive monetary shock does stimulate economic activity temporarily, once everything plays out economic activity will return to its previous level and only prices will rise permanently. By then, of course, Trump may have been reelected. But this is precisely why we have given our central bank relative independence; to prevent politicians who are up for reelection from manipulating monetary policy for political gain at the expense of everybody else. If the President wants sustained improvement in economic activity, he should rethink his trade policies. But I am afraid there is something even worse happening here.

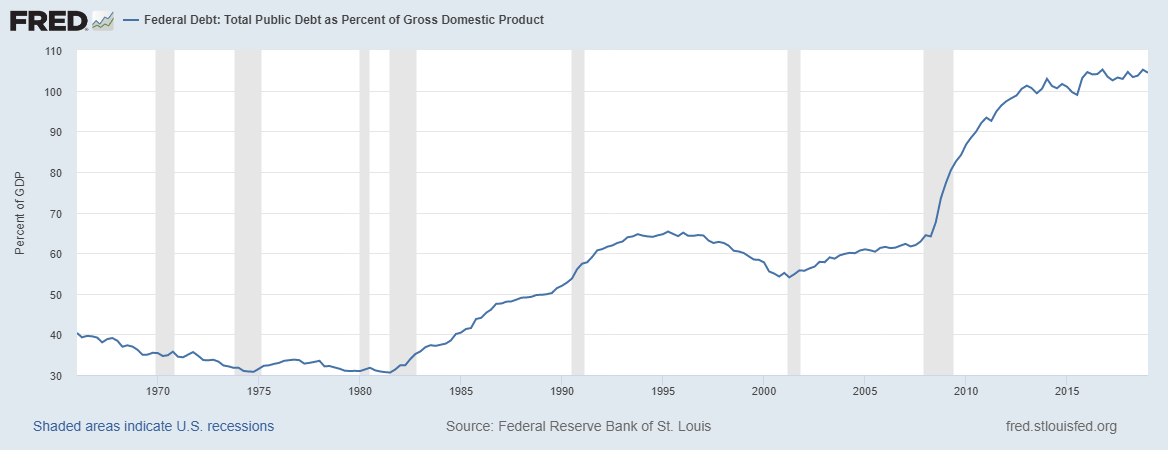

In the press conference, Trump laid out a plan for further cuts in payroll and capital gains taxes. The announcement came just in time for the 2020 elections. Isn't a tax cut a good thing? Well, not if it is not followed by curbing spending and is accompanied by a historically high debt and large budget deficits about to make the debt grow further. As the graph below shows, the Federal government debt as a percent of GDP is currently at 104.5%, the highest it has been since the end of WWII.

Making matters worse, as shown below, the federal government is running the highest budget deficit as a percent of GDP during a boom since WWII. The budget deficit was larger during the early 1980s and during the Great Recession, but this is to be expected following an economic downturn (the shaded eras). If the deficit is so large when the economy is booming, what would happen if we entered a recession?

To finance his new tax cuts, Trump needs the Fed to keep interest rates low and to keep buying Treasuries, which means maintaining a large balance sheet. So long as the Federal government can keep borrowing at extremely low interest rates, the government debt can remain sustainable even if it grows further. If interest rates rise however, well, let's just say that nightmares of Greece haunt me. Of course, unlike Greece, the US has a central bank with an unlimited supply of money that it can use to keep buying government debt that nobody else wants to buy at high prices. But then, it is a matter of time before inflation starts creeping up. Trump may be reelected and gone by then, but the rest of us will still be here trying to clean up the mess.